Finding the best car insurance renewal quotes in 2026 starts with mastering your No Claim Bonus (NCB). Whether you are looking to buy comprehensive car insurance online or switch for a better claim settlement ratio, your NCB is your biggest bargaining chip for massive savings.

It can reduce your own-damage premium by 20% to 50%, which is the secret to getting the cheapest car insurance renewal quotes in 2026.

If you own a car in India, this is one of the easiest ways to save on renewal without lowering your cover. The key is simple: drive carefully, avoid unnecessary claims, and protect your bonus when needed.

No Claim Bonus Explained

NCB full form is No Claim Bonus, and it is a reward insurers give when you do not file a claim during the policy term.

The bonus is linked to the policyholder, not the car, so you can carry it when you change your vehicle or insurer. It generally applies only to the own-damage part of your premium, not the mandatory third-party premium.

Where NCB Applies

NCB reduces the part of the premium that covers damage to your own car. That means even a strong NCB will not reduce the fixed third-party premium in a comprehensive policy. This is why many car owners track own-damage premium carefully at renewal.

How NCB Works in India

The standard NCB slab in India starts at 20% after one claim-free year and rises with each consecutive claim-free year.

After two years it is 25%, after three years 35%, after four years 45%, and after five years 50%. Once you reach the maximum, the discount usually caps at 50%.

Year-Wise Discount Slab

| Claim-free years | NCB discount |

|---|---|

| 1 year | 20% |

| 2 consecutive years | 25% |

| 3 consecutive years | 35% |

| 4 consecutive years | 45% |

| 5 consecutive years | 50% |

This structure is why long claim-free ownership can create meaningful savings over time. For many drivers, NCB becomes the easiest premium-saving lever at renewal.

Top Car Insurance Providers for NCB & Claims (2026)

| Insurer | Claim Settlement Ratio (2025-26) | Cashless Garage Network | Key NCB Benefit |

|---|---|---|---|

| Reliance General | 100% | 11,000+ | Up to 90% discount on online premiums |

| HDFC ERGO | 99% | 8,700+ | Overnight vehicle repairs & doorstep service |

| TATA AIG | 99% | 10,000+ | 13+ customisable add-ons for high-end cars |

| SBI General | 98% | 16,000+ | Widest network; backed by India’s largest bank |

| Digit Insurance | 96% | “Repair Anywhere” | Digital-first, zero-paperwork claim process |

Why the bonus increases yearly

Insurers use NCB to reward low-risk driving behavior. A claim-free record signals fewer payouts and better loss control, so the insurer shares part of that benefit with you. This also discourages filing tiny claims that may cost more in lost discount than the repair itself.

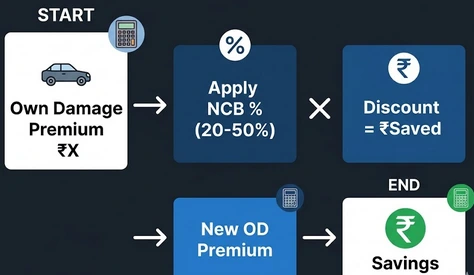

How to Calculate NCB

The calculation is simple: apply the NCB percentage only to the own-damage premium.

Formula: NCB discount = Own-damage premium * NCB percentage.

Then subtract that amount from the own-damage premium to get the renewal price.

Example with own damage premium

Suppose your own-damage premium is ₹12,000 and you have 35% NCB. Your discount is ₹4,200, so you pay ₹7,800 for the own-damage part before taxes and other charges. If the third-party premium is separate, it remains unchanged.

Quick Savings Check

- 20% NCB on ₹10,000 OD premium = ₹2,000 saved.

- 35% NCB on ₹15,000 OD premium = ₹5,250 saved.

- 50% NCB on ₹20,000 OD premium = ₹10,000 saved.

When NCB is lost or reduced

A claim usually resets your NCB to zero, an NCB Protector add-on (costing roughly 5-10% of the premium) allows 1–2 claims without losing the 20%–50% discount.

That is why even a small claim can become expensive in the long run.

A break in renewal can also create risk, because continuity matters for keeping the benefit. Top providers like ICICI Lombard and Bajaj Allianz offer multi-claim protection that pays for itself after just one minor accident.

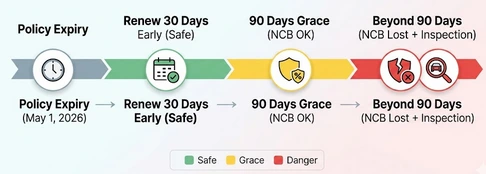

Policy expiry and grace period risk

IRDAI-linked guidance shared by insurers says renewal should happen before expiry to keep continuity, and delay beyond the permitted window can cause NCB loss.

So, the safe habit is to renew early and keep records ready. This is especially important if you are switching insurers near expiry.

How to Transfer NCB

Transferring your 50% NCB from an old Maruti to a new luxury car? You can carry your bonus even if you switch from a public insurer like New India Assurance to a private one like Acko for faster digital service

For online renewal, insurers usually ask for the previous policy number, prior insurer name, and correct NCB percentage.

For offline transfer, you may need an NCB certificate or retention letter from your old insurer.

Transfer Steps

- Ask your old insurer for the NCB certificate or retention letter.

- Keep your previous policy details and renewal date ready.

- Share the correct NCB percentage with the new insurer.

- Check that the new policy reflects the transferred bonus before payment.

Documents to Keep

- Previous policy copy.

- NCB certificate or retention letter.

- Sale documents or ownership transfer papers when changing cars.

- Basic ID and policy details.

NCB Protector and Smart Ways to Retain Bonus

An NCB protector add-on helps you keep your discount even after a claim, depending on policy terms.

This is useful for drivers who want premium stability and may face one unavoidable claim.

It can be a smart add-on when your car’s own-damage premium is high and the NCB value is meaningful.

When protector helps

- You drive daily in dense traffic.

- Your car repair bills are usually high.

- You want to avoid losing a strong NCB for one claim.

When to avoid small claims

- Do not file a very small claim if your future NCB loss is bigger.

- Do not let the policy lapse before renewal.

- Do not assume third-party premium gets discounted by NCB.

2026 Renewal Checklist

Use this quick checklist before renewal:

- Check your current NCB percentage.

- Confirm whether you had any claims last year.

- Compare own-damage premium separately from third-party premium.

- Ask for NCB transfer documents if changing insurer.

- Consider NCB protector if one claim could hurt future savings.

This checklist is useful for both first-time buyers and long-term policyholders. It keeps the renewal process clean and avoids accidental loss of discount.

Frequently Asked Questions: Maximizing Your 2026 Car Insurance Savings

While the NCB slab is standardized by IRDAI, insurers like HDFC ERGO and Tata AIG are highly rated for 2026 because they offer robust NCB Protector add-ons and a high Claim Settlement Ratio, ensuring your discount remains secure even after a minor accident.

Absolutely. Your No Claim Bonus is portable. When you compare car insurance quotes online, you can transfer your accumulated 20%–50% discount to a new provider like Digit or Acko to lower your premium further.

A claim usually resets your No Claim Bonus (NCB) to 0%, causing you to lose your accumulated discount for the next renewal. However, you can buy an NCB Protector add-on. For a small additional premium, this protector ensures that one minor claim won’t reset your bonus, potentially saving you between ₹5,000 – ₹15,000 on your next renewal.

No. NCB only applies to the Own-Damage (OD) premium. It does not reduce the mandatory Third-Party Insurance cost or the cost of other add-ons like Zero Depreciation or Consumables cover.

To keep your NCB intact, you must renew your policy within 90 days of the expiry date. If you fail to renew within this window, your bonus resets to 0%, regardless of how many claim free years you had.

No claim bonus in car insurance is a renewal discount you earn for staying claim-free during the policy term. It lowers the own-damage part of your premium and rewards careful driving.

In India, NCB usually starts at 20% after one claim-free year and can rise to 50% after five consecutive claim-free years. The discount is usually capped at 50%.

No, NCB generally applies only to the own-damage portion of your car insurance premium. The mandatory third-party premium stays fixed and is not reduced by NCB.

Yes, NCB is attached to the policyholder, so you can transfer it when you buy a new car. You usually need policy details and an NCB certificate or retention letter from the previous insurer.

Take the own-damage premium and multiply it by your NCB percentage. For example, if your OD premium is ₹10,000 and NCB is 25%, your savings are ₹2,500.

Yes, in most cases an NCB certificate or retention letter helps prove your claim-free record. It makes transfer to a new insurer or vehicle smoother and reduces the chance of rejection.

In 2026, No Claim Bonus in car insurance remains the most effective way to keep your ownership costs low. However, the secret to the best deal isn’t just accumulating the bonus – it’s protecting it. By choosing a comprehensive policy with an NCB Protector and selecting an insurer with a vast cashless garage network, you ensure that your savings are never compromised by a single unfortunate event.

Before you renew, always compare the own-damage premiums across top-rated providers. Whether you are transferring a certificate to a new vehicle or switching to a digital-first insurer for better service, your NCB is your most valuable asset.