As a Professional Insurance Advisor (IRDAI‑authorized) specializing in comprehensive general insurance and risk management in India, I see the same question repeatedly: Should I buy third‑party or comprehensive car insurance?

The answer depends on your car’s age, usage, and how much repair risk you can afford. In 2026, rising third‑party tariffs and evolving IRDAI rules make this choice even more critical.

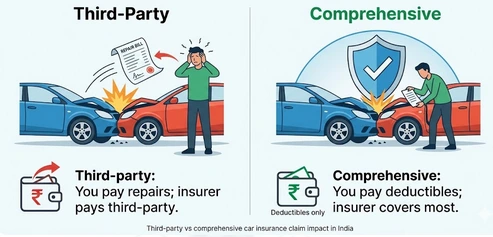

What third‑party car insurance covers

Third‑party car insurance is the minimum legal cover required under the Motor Vehicles Act, 1988. It protects you against financial liability to:

- Third‑party bodily injury or death

- Damage to third‑party property (car, building, etc.)

However, it does not pay for damage to your own vehicle, so your own repair bill comes out of pocket.

For an Indian car owner, this means third‑party insurance keeps you legally compliant but not financially protected for your own car.

What comprehensive car insurance covers

Comprehensive car insurance blends third‑party liability + own‑damage cover in one policy. In India, it typically includes:

- Third‑party injury, death, and property damage

- Own‑damage from accidents, fire, theft, and many natural calamities (subject to exclusion)

- Optional add‑ons like zero‑depreciation, roadside assistance, engine protect, and NCB‑protect

Because of this, comprehensive insurance is closer to “full‑stack” protection for the car, driver, and third parties.

Third‑party vs comprehensive: key differences

| Feature | Third‑party car insurance | Comprehensive car insurance |

|---|---|---|

| Legal requirement | Mandatory in India | Optional, not mandated by law |

| Own‑damage cover | Not covered | Covered (subject to exclusions) |

| Theft & natural calamities | Not covered | Generally covered |

| Add‑ons | Not available | Yes (zero‑depreciation, roadside, engine, etc.) |

| Premium | Lower, IRDAI‑regulated bands | Higher, based on IDV, add‑ons, and risk factors |

In simple terms:

- Third‑party = you protect others

- Comprehensive = you protect others + your car

Which is better: third‑party or comprehensive car insurance in India?

The best choice depends on four key factors:

- Age and value of the car

- How often you drive

- City risk (traffic, theft, flood)

- Your ability to bear repair costs

Here is how I advise clients in Hyderabad and across India:

For new cars (≤3 – 5 years)

For a new car, especially one with high‑value components or financed loans, comprehensive car insurance with zero‑depreciation is usually the smarter choice.

Why?

- Repair bills, especially for newer models, can quickly cross 1.5–2 lakh even for a moderate accident.

- Zero‑depreciation reduces out‑of‑pocket costs on consumable parts and plastic, which would otherwise be discounted at claim time.

If your car is new, you drive daily, or you park in a high‑traffic area, third‑party vs comprehensive car insurance leans strongly toward comprehensive.

For old cars (7+ years)

For older cars with low market value and low usage, many owners shift to third‑party insurance only.

Typical reasoning:

- Repair cost of an old car may be close to or higher than its resale value, so paying a high own‑damage premium becomes irrational.

- As long as the car is still road‑legal and not used heavily, third‑party insurance for old cars in India can be a cost‑efficient, compliance‑focused option.

However, if your old car is in a high‑theft or flood‑prone area, comprehensive coverage may still make sense.

For heavy daily / city driving

If you drive every day in a city (for work, deliveries, or rideshare‑style use), accident exposure is higher.

In such cases, I recommend:

- Comprehensive insurance as the default

- Zero‑depreciation and roadside assistance if your budget allows

This combo reduces:

- Out‑of‑pocket repair shock after a minor collision.

- Inconvenience and towing costs if the car breaks down.

For occasional or low‑use vehicles

If the car is parked for weeks and driven only on weekends or holidays, third‑party vs comprehensive car insurance tips tilt toward third‑party.

Common scenario:

- Family’s second car, used only for long‑distance trips or festivals.

- Older sedan, low odometer, and minimal city‑driving risk.

Here, the goal is legal compliance at the lowest sustainable premium, not full asset protection.

2026 India updates you must know

India’s third‑party car insurance landscape is changing in 2026, and this affects your decision:

- Third‑party premium movement:

- IRDAI‑linked third‑party tariff bands have been revised upward in recent years, and further increases are under discussion to keep pace with injury‑compensation trends.

- Why premiums change:

- Rising medical costs and accident‑severity.

- Higher compensation norms for third‑party bodily injury.

- Risk‑based capping by engine class and vehicle type.

- What you should do now

- Compare premium vs expected repair cost, not just the lowest number.

- Check whether your insurer offers competitive own‑damage pricing and add‑on stacking (zero‑depreciation + roadside) before deciding on a pure third‑party plan.

Claim impact and common exclusions

What third‑party insurance does not pay for

Because third‑party insurance only covers someone else’s loss, it never pays for:

- Your car’s bodywork, dents, or mechanical damage.

- Your own medical bills, unless you have a separate personal health or personal accident cover.

- Towing or storage charges arising from your loss.

This is why many owners realize too late that “the cheapest policy” left them with a huge repair bill after an accident.

What comprehensive insurance may still reject

Comprehensive policies are broader, but they still exclude claims arising from:

- Drunken driving or driving under intoxication.

- Driving without a valid licence.

- Driving in an unauthorized or non‑road use (e.g., unauthorized track use).

- Deliberate or fraudulent incidents.

Also, deductibles and depreciation apply in many cases, unless you have a zero‑depreciation add‑on.

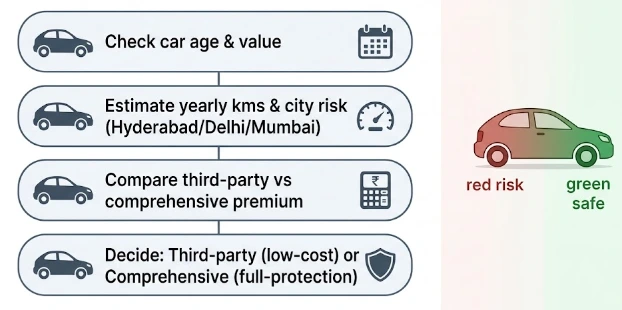

How to choose between third‑party and comprehensive car insurance in 5 steps

Use this checklist before renewal:

- Check your car’s real market value

- Use the insurer’s IDV calculator to see current market value after depreciation.

- If repair cost is higher than 40–50% of IDV, comprehensive becomes more important.

- Count your yearly mileage and city risk

- High‑traffic city (Hyderabad, Delhi, Mumbai) → higher accident risk → more reason to choose comprehensive.

- Low‑mileage, rural or semi‑urban use → third‑party may suffice.

- Compare premium and add‑on combos

- Take a third‑party only quote vs a comprehensive + zero‑depreciation + roadside quote.

- Decide if the extra 15–25% premium is worth the peace of mind.

- Review your risk appetite

- Will you pan‑out 1–2 lakh for a major accident from your savings?

- If not, comprehensive insurance is usually the safer helmet.

- Avoid these common mistakes

- Never confusing third‑party insurance with full coverage.

- Never skipping NCB or zero‑depreciation on a new car just to save 10–15k per year.

- Never assuming your car is too old to insure – older cars can still need third‑party or limited OD.

When to strongly prefer comprehensive Insurance

- Newly purchased car (0–3 years).

- Car financed by a bank or NBFC.

- Daily commute in a metro city.

- High‑end or premium model (SUV, luxury sedan).

- Owner who wants cashless garage repairs and hassle‑free towing.

In these cases, third‑party vs comprehensive car insurance is not really a debate: comprehensive is the logical default.

When third‑party insurance may be enough

- Old car (7–10+ years) with low resale value.

- Car used only for occasional trips, not daily driving.

- Tight budget, where even a moderate OD premium strains finances.

- You have a separate contingency fund and can afford one‑time repair or replacement.

For such scenarios, third‑party insurance for old cars in India can be a practical, legally compliant option.

Yes, third-party insurance is mandatory under Indian motor law for all vehicles on public roads. It exists to protect accident victims and ensure liability is financially covered. A car without it can face legal and financial trouble.

Comprehensive car insurance generally covers third-party liability plus damage to your own vehicle. Depending on the policy, it may also include theft, fire, and natural calamities. Final protection depends on exclusions, deductibles, and chosen add-ons.

A new car usually fits comprehensive insurance better because repair costs, part replacement, and depreciation exposure are higher. Owners also gain access to useful add-ons that reduce claim stress. This makes the policy more suitable for early ownership years.

It can be enough when the car has low market value and limited usage. The idea is to avoid paying a high premium for protection that may exceed the car’s worth. Still, theft, flood, and repair risk should be checked before dropping own-damage cover.

It costs more because it covers a wider risk pool and often includes add-ons. Premium pricing also depends on the car’s IDV, model, and selected protection level. You pay more, but you also shift more financial risk to the insurer.

Zero depreciation is usually an add-on linked to comprehensive insurance, not third-party insurance. It is especially useful for newer cars because it can reduce deductions during claims. Eligibility and age limits depend on the insurer and vehicle profile.

Match the policy to the car’s value, how often you drive, and how much repair risk you can absorb. If the car is new, expensive, or used daily, comprehensive is usually the stronger option. If the car is older and lightly used, third-party insurance can be a cost-smart minimum cover.

Conclusion: Third-party vs comprehensive car insurance is really a choice between minimum compliance and wider protection. If your car is new or valuable, comprehensive usually offers better peace of mind. If your car is old and low-value, third-party insurance may be the more practical route.