Comprehensive car insurance India front-loads protection beyond mandatory third-party cover. It shields your vehicle from own damage, theft, and calamities. As an IRDAI-authorized agent with 10+ years of experience, I’ve seen it save families lakhs in unexpected repairs.

India’s roads see rising accidents – motor insurance market hits USD 3.67B in 2026, growing 11.52% CAGR. This policy combines third-party liability with own damage (OD). You pick Insured Declared Value (IDV) – your car’s market worth minus depreciation per IRDAI.

What is Comprehensive Car Insurance?

Comprehensive car insurance in India bundles own damage and third-party liability. IRDAI mandates third-party but makes OD optional, yet essential for full safeguard.

It pays for your car’s repairs if at fault, unlike basic plans. Premiums factor IDV, age, location. Example: Rs 8L IDV car might cost Rs 15-20K yearly.

I had checked many cases where floods wrecked sedans – claims settled fast via IDV.

Coverage Details

Comprehensive car insurance coverage India includes:

- Own Damage: Accidents, fire, explosion, theft (up to IDV).

- Third-Party Liability: Injury/death (Rs 15L owner-driver), property damage (unlimited).

- Natural Calamities: Floods, cyclones, earthquakes – key in monsoon-hit areas.

- Man-Made Risks: Riots, strikes, terrorism.

- Animal Hits: Stray cows common in India.

- Transit Damage: While shipping vehicle.

Personal accident cover mandatory at Rs 15L for owner-driver. Real case: 2025 Hyderabad hailstorm – policy covered Rs 2L glass repairs fully.

Comprehensive vs Third-Party Car Insurance India

Choose comprehensive for cars under 15 years – protects investment.

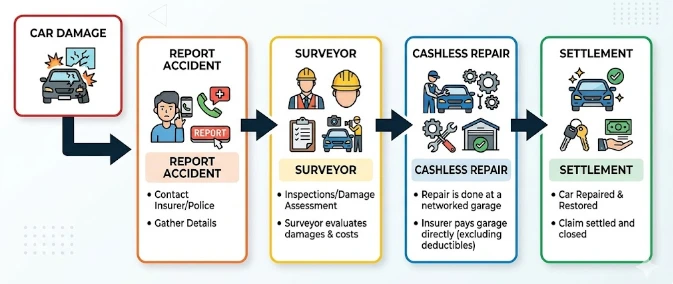

How Comprehensive Car Insurance Claims Process Works India

Comprehensive car insurance claims process India follows IRDAI timelines.

Step-by-Step (Cashless at 8,000+ network garages like HDFC ERGO):

- Report Immediately: Call insurer within 24hrs. FIR if theft/damage >Rs 10K.

- Surveyor Appointed: Within 24-72hrs. Inspects in 48hrs.

- Repair Estimate: Garage quotes. Pay compulsory deductible (Rs 500-5K).

- Approval: Insurer approves in 15 days max.

- Repair & Settlement: Cashless repair. Settle within 30 days of docs.

Reimbursement: Fix elsewhere, submit bills.

What Not to Do: Delay FIR – rejects 20% claims. Drive drunk – voids policy.

Real case: Client totaled SUV in riot; IDV Rs 12L paid minus salvage.

2026 Tip: Video claims for spot approval up to Rs 20K (Digit, Bajaj).

Benefits of Comprehensive Car Insurance India

Key benefits:

- Peace of mind – covers 80% risks vs third-party’s 20%.

- No Claim Bonus (NCB): 20% year 1, up to 50% year 5. Transferable.

- Add-ons boost: Zero depreciation (no age cut), RSA (24/7 tow), engine protect (water ingress).

- Tax save u/s 80C.

India stats: 99% CSR for top insurers like HDFC ERGO. As SME, add-ons saved my clients 30% post-flood.

Exclusions and Insider Tips

Exclusions: Drunk driving, wear-tear, unlisted mods.

Checklist for Comprehensive Car Insurance:

- Verify IDV (avoid under-insure).

- Pick 50+ NCB if switching.

- Add zero dep for new cars.

- Renew 60 days early – no break.

- Park in garage for lower premium.

Employee Tip: Use IRDAI portal for complaints – resolves 90% in 15 days.

2026 IRDAI Comprehensive Car Insurance Rules Updates

IRDAI 2026 mandates: Survey in 48hrs, settle 30 days, RC submit for total loss. UBI (pay-per-km) pilots for low-mileage drivers. NCB grid standardized across insurers. CSR data: Acko leads at 99%+.

Market grows to USD 6.33B by 2031.

Conclusion: Comprehensive car insurance India works via IDV-backed claims for total protection. It beats third-party for real-world risks.

Get free quote – compare top insurers.

Renew before lapse for NCB retention.

Chat for personalized add-ons advice.

No, only third-party is mandatory per Motor Vehicles Act. Comprehensive adds OD voluntarily for better protection.

IDV is your car’s depreciated market value – base for theft/total loss payouts. IRDAI sets dep: 50% after year 5.

No Claim Bonus (NCB) starts at 20% premium discount after one claim-free year, rising to 50% by the fifth year under comprehensive policies. It applies only to own damage premiums, resets fully on claims but partially protects third-party portions per IRDAI norms.

Yes, IRDAI mandates full NCB transferability when switching insurers for comprehensive car insurance. Submit your previous policy and renewal documents as proof during the new quote process to retain up to 50% discount without any loss in accumulated benefits.

If repair costs surpass 75% of IDV, insurers declare it a total constructive loss under IRDAI rules. You receive full IDV payout minus salvage value, with options to keep the wreck by deducting its worth or surrendering it for cashless settlement.

Base comprehensive car insurance excludes roadside assistance like towing or flat tire fixes. Purchase it as an add-on rider for 24/7 services including fuel delivery, battery jump-starts, and taxi support up to specified limits, ideal for breakdowns on highways.

Yes, premiums for comprehensive car insurance rise significantly in high-risk zones like Delhi or Mumbai due to theft and accident stats. IRDAI zonal pricing adds 20-30% extra in metro areas versus Tier-2 cities, factoring vehicle parking security and crime data.